It’s been a bad year for news headlines, but a great year on the institutional fundraising frontline.

You could be forgiven for thinking that the private credit market has suffered the worst period in its history, with doom and gloom implied by countless headlines in the mainstream press. Whether it’s the redemption rush, assumed AI disruption or portfolio stress, the talk of the asset class’s “golden era” that surfaced a few years back strikes a sharp contrast with today’s reality.

Or does it? Maybe it is in fact time to bring back that hype and for everyone to cheer up a little. The provisional Private Debt Investor fundraising figures for the first half of this year show that, from an institutional fundraising perspective, private credit has never had it so good. While the figures are subject to some adjustment, the general trend will almost certainly not be – institutions, focused on long-term prospects rather than short-term concerns, are propelling the asset class to a likely record-breaking year for fresh capital.

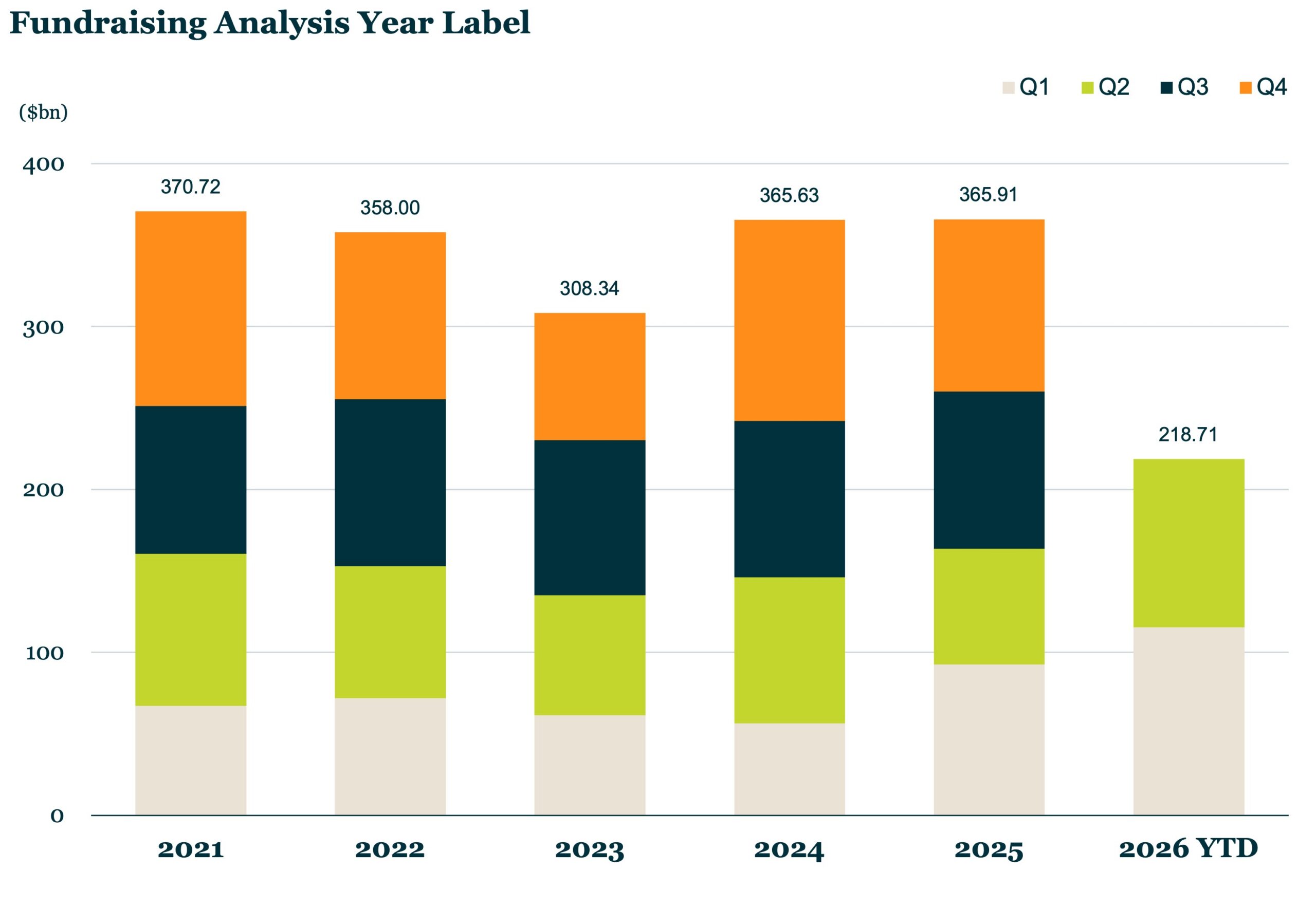

As can be seen from our accompanying chart, the second quarter saw over $103 billion raised, following on strongly from the more than $115 billion raised in the first quarter. The total for the first half of almost $219 billion puts 2026 well on track to beat the annual record of almost $371 billion raised in full-year 2021.

When it comes to the number of funds raised, it’s a completely different story. This year has seen 215 vehicles reach a final close so far, compared with 255 at the same stage last year and 315 in the record year of 2021. This appears to further underline the ongoing trend of private credit’s GP heavyweights raising ever-larger funds.

One thing is clear: there is now a sharp divide between the appetite of US retail investors for the asset class and that of global institutional LPs. While the former have been fleeing for the hills, the latter are piling into private credit as never before.

Latest news

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…