Private credit fund redemptions have put semi-liquid, evergreen funds firmly in the spotlight.

The three “Bs” – Blackstone, BlackRock and Blue Owl – have all found themselves at the centre of media coverage focused on investor redemptions. This in turn prompts urgent consideration of the suitability of private credit vehicles – and private market vehicles in general – for what is expected to be an upsurge in commitments from retail investors.

In its 2025 Market Overview, Hamilton Lane said: “Our view is that evergreen structures will come to form a major part of the private markets landscape in a very short time frame”. Evergreen funds are primarily associated with retail investors (though may include institutional investment as well).

But while Hamilton Lane forecast this rapid increase in evergreen funds, it also provided what looks to have been a prescient warning. It gave a 75 percent chance of the following event happening: “There is a market decline or major event that causes most evergreen funds to gate investors”.

We may not yet be at the point where MOST funds are affected, but gating has certainly made itself apparent and garnered some not entirely flattering headlines.

These developments come at a crucial time, given predictions of vast inflows of retail capital into private markets. Deloitte last year predicted, that should current trends continue, retail investor allocations to private capital will – from 2024 to 2030 – grow from $80 billion to $2.4 trillion in the US and from €924 billion to €3.3 trillion in the European Union.

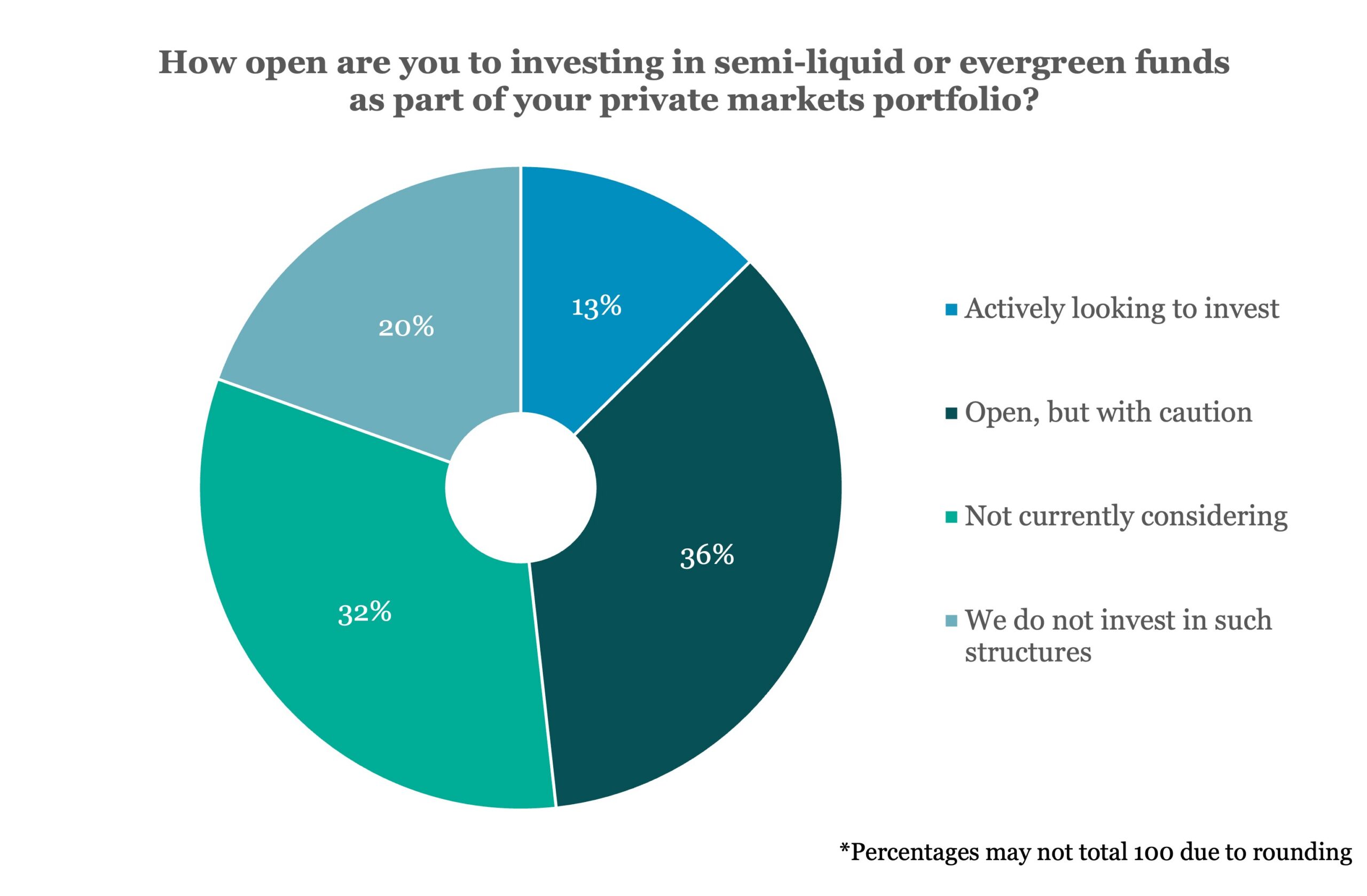

In our own LP Perspectives 2026 study, we discovered 49 percent of private market investors canvassed were either actively looking to invest in evergreen funds or were open to investing, but with caution (see accompanying chart).

With the appetite from retail investors clear, the challenge for private credit and other alternative asset classes is to make sure they are fully educated about the nature of what they are investing in and that the structures created to accommodate the capital are able – as far as possible – to meet the needs and expectations of both investor and fund manager.

Latest news

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…