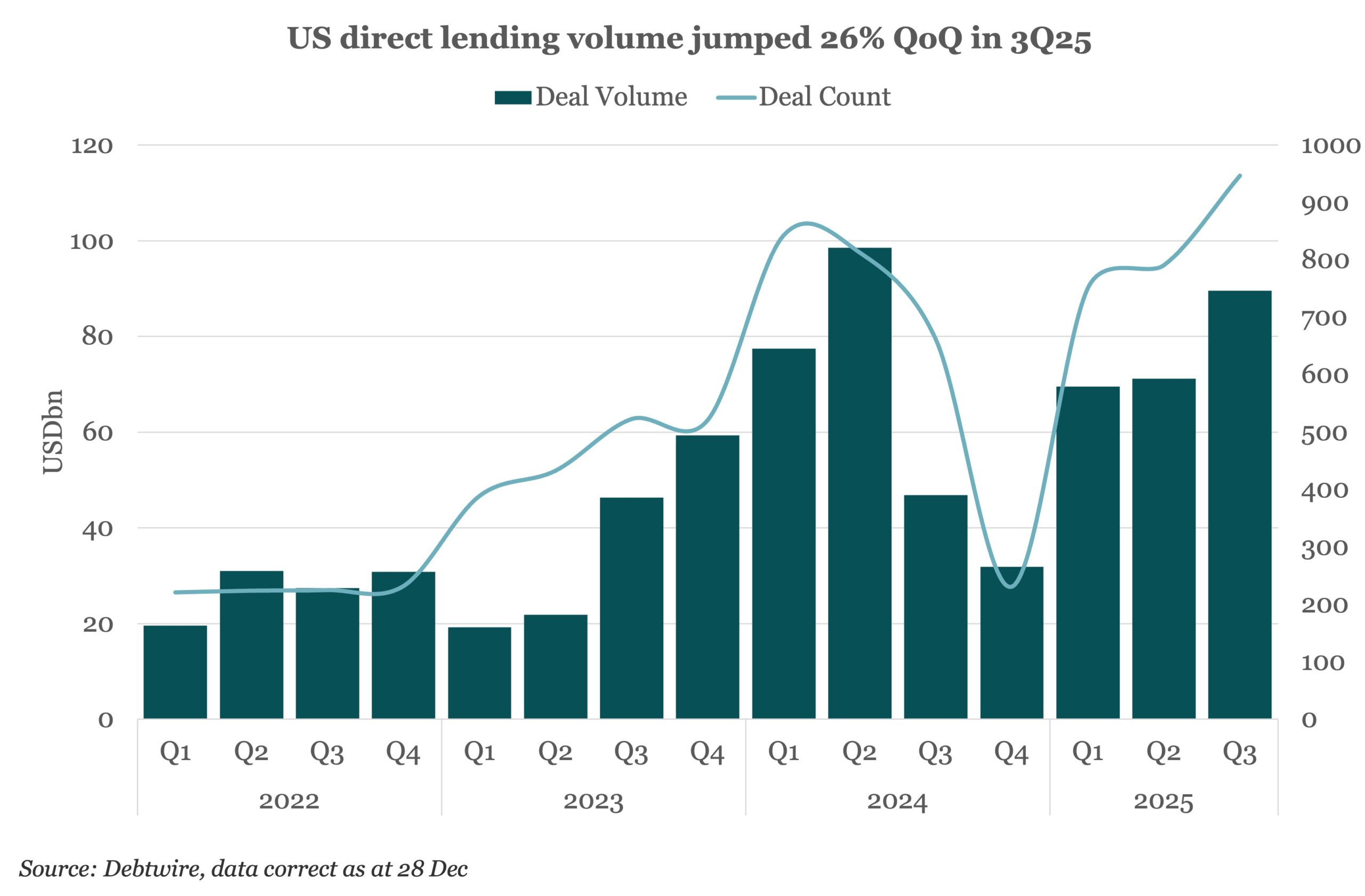

Direct lending volumes saw a substantial rise in 3Q25, climbing 26% quarter-on-quarter (QoQ) to USD 89.5bn from USD 71bn in 2Q25. Deal activity also increased, rising from 791 transactions in 2Q25 to 947 in 3Q25. The volume in 3Q25 was the second-highest quarter on record, narrowly trailing 2Q24’s USD 98.5bn, according to Debtwire data.

“This trend is likely driven primarily by the implications of ‘Liberation Day’ and the uncertainty around tariffs and macroeconomic activity,” said a private lender. “The market – both sponsors and lenders – put transactions on hold in 2Q25 that had any tariff exposure until there was more certainty on how that would all play out. In 3Q25, we saw activity begin to pick up again. We also observed this trend, although we were strategic and constructive through both 2Q25 and 3Q25 on finding strong, tariff-insulated credits to invest in.”

Direct lending funded LBO rise in 3Q25

Leveraged buyouts (LBOs) funded by direct lending began 2025 on a strong footing, generating USD 23.3bn in volume in 1Q25, before falling sharply to USD 13bn in 2Q25. Activity rebounded decisively in 3Q25, climbing 74% QoQ to USD 22bn, making up for 25% of overall volume for the quarter. In contrast, institutional leveraged loans saw minimal LBO activity in 3Q25, with LBOs accounting for just 1% (USD 3.9bn) despite the substantial issuance of USD 376bn in the quarter.

Prominent direct lending deals funding LBO transactions in 3Q25 included a USD 1.2bn private credit loan package to fund private equity firm GTCR’s USD 2.5bn leveraged buyout of smart home security provider Simplisafe, and a USD 1.17bn loan package backing EQT’s USD 3bn leveraged buyout of HR software provider Neogov.

Refinancing boosts third quarter activity

LBO activity was not the sole driver of the third quarter rebound. Refinancing volumes continued to grow steadily throughout the year, increasing each quarter and reaching a total volume of USD 37bn in 3Q25, up from USD 23bn in 1Q25.

“The rise in refinancing activity can be attributed to the fact that sellers continued to hold on to assets longer, given selling valuation multiples were not where they desired, and instead opted for refinancing, often extending maturity and repricing the loans to market levels – which had declined since the original deal was made – and will re-evaluate selling when the market is more receptive” the private lender added.

The next largest use of proceeds volume – M&A-related direct lending activity – contrasted refinancing and LBOs by remaining relatively stable in 3Q25, with volumes holding around USD 11bn in both the second and third quarters of 2025.

Outlook for 2026

There are additional signs of growth in direct lending activity in 2026. Debtwire tracked USD 145bn in US-focused direct lending fundraising in 2025 – the highest amount on record – leaving substantial dry powder available to fund the growing surge of M&A activity and associated debt financing needs in the year ahead.

“My outlook is positive,” said the private lender. “However, there is still a large amount of direct lending capital that lenders are looking to deploy. This is resulting in increased competition for assets, which tightens pricing and loosens terms.”

The increased competition and plentiful capital works in favor of the borrowers, undoubtedly leaving some direct lenders unable to compete. The private lender added that “a key trend over the next couple of years will be determining who wins and who loses, with the expectation that scaled players will continue to gain market share and prevail over smaller or new entrants.”

For access to our comprehensive news, analysis and data on the global loan and bond markets, please subscribe to Debtwire.

(Past performance is no guarantee of future results.)

Contact: Jayjeet Sharma

jayjeet.sharma@iongroup.com

Latest news

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…