One of the many benefits of business development companies is their ability to easily hold a wide range of investments. From senior term loans, to unitranche loans, second-lien term loans, mezzanine debt, and even preferred stock, BDCs are incredibly versatile asset management vehicles.

Historically, BDCs allocated more capital to higher-yielding, thus more risky, assets; particularly junior capital. This made sense given that relatively low 1:1 leverage helps protect investors from swings in asset values. It also suited BDCs’ higher return parameters. In the early 2000’s, mezz was a good place to play in the capital structure.

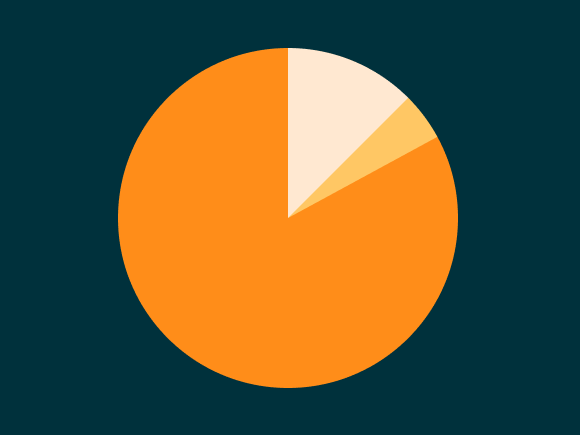

After the Great Recession, BDCs began to climb the capital stack. As our Chart of the Week showcases, the bulk of BDC assets are now comprised of first and second-lien loans. Since the end of last year, the share of those loans has grown, while the concentration on subordinated debt and equity has shrunk.

BDC managers, of course, are reacting to current loan market conditions as are other fund managers. Those trends are favoring issuers of all-senior debt structures, in all their permutations, rather than the classic senior/sub mix.

This despite the fact that including mezzanine debt as patient capital in private equity sponsored transactions typically allows total leverage to be pushed higher than those without non-amortizing tranches. Today both first-lien/second-lien and unitranche options are actually sporting higher leverage in middle market deals.

Every BDC has its unique investment parameters. While the senior debt versions seek first-lien, cash flow term loans, most still target higher yielding assets. This distinguishes them from middle market finance companies, credit op funds, and banks.

Thomson Reuters LPC reports all-in middle market institutional yields are presently hovering around 6%. Unitranches, by contrast, weigh in at 7.5%, and second-lien term loans are just below 10%. But higher leverage means higher risk. The question, of course, is whether BDC investors are being paid sufficiently for that risk.

That’s just the kind of decision those investors select an experienced manager to make. In this aggressively sell-side friendly market, it’s difficult to tell which borrowers deserve favorable terms, and which don’t.

It’s not just specific investment decisions that matter in building a superior track-record. Portfolio mix counts as well. Overweighting on second-lien in this market, as leverage multiples continue to rise, is tricky business. When the inevitable downturn arrives, maintaining reasonable loan to value ratios will separate BDC winners from losers.

Next week: How public BDCs are faring in the current market.

Latest news

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…