Download PitchBook’s Report here.

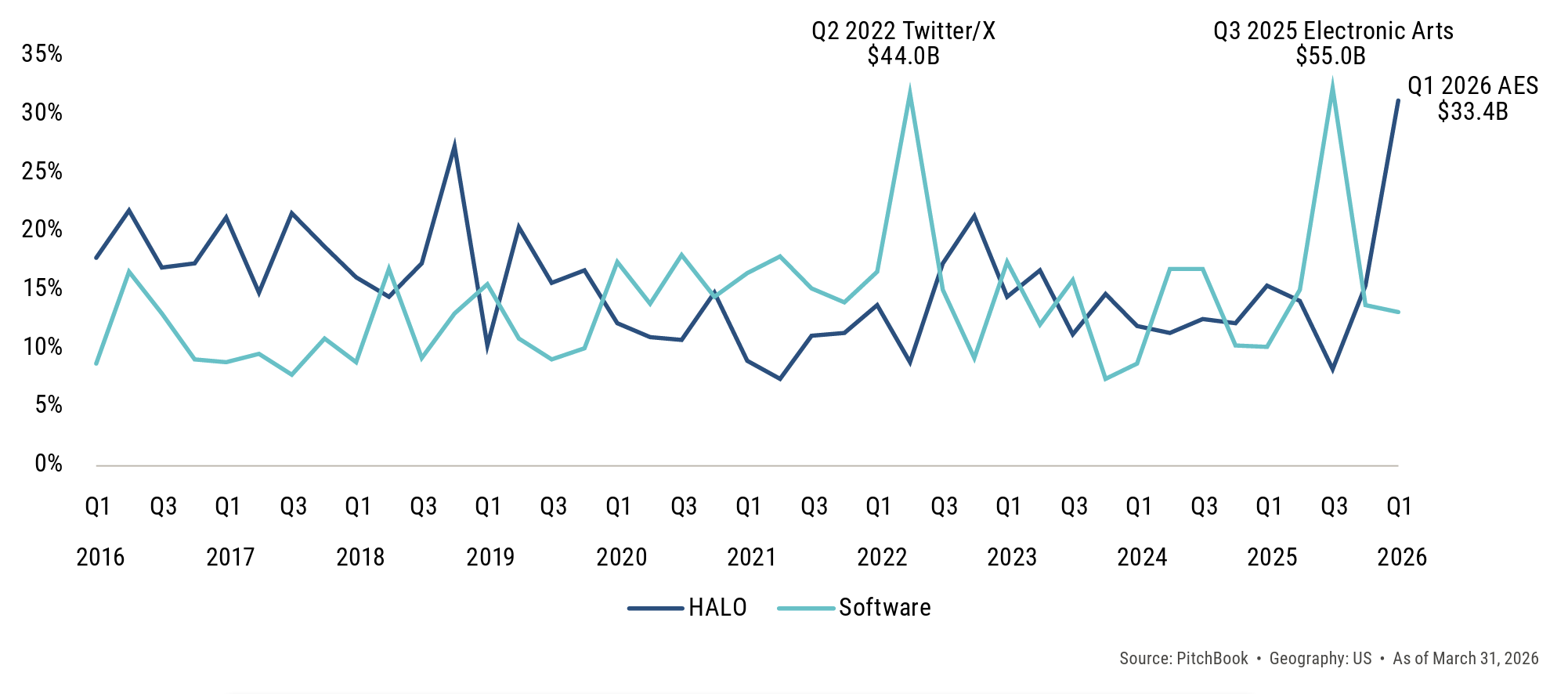

The hottest debate in public markets right now is not whether AI will disrupt software but how much, how fast, and who is left standing. In search of shelter, investors have rotated toward what has come to be called the “HALO” trade: Heavy Assets, Low Obsolescence, a term coined by Josh Brown, CEO of Ritholtz Wealth Management. The thesis is straightforward. Companies built on transmission grids, pipelines, utilities, transport infrastructure, and long-cycle industrial capacity own assets that are costly to replicate, slow to depreciate, and largely indifferent to whether the next AI model ships in six months or six weeks. These same companies stand to benefit from AI on the cost side, as robotics and smart monitoring systems reduce labor expenses and increase uptime. Private market investors have been active in these categories for years and are positioned to lean in further. To quantify the shift, we screened over 82,000 PE deals from Q1 2016 through Q1 2026 across seven top-level sector categories, filtering for 40 HALO subsectors spanning energy, materials, chemicals, heavy industrials, and primary production assets. What emerged was a decade-long pattern hiding in plain sight. From 2016 through 2024, HALO deals accounted for a steady 10% to 15% of PE deal count and roughly 14% of capital deployed: consistent, underloved, and largely unremarked upon as software commanded the headlines and the multiples. Then came the inflection. In Q1 2026, HALO captured 31.2% of all PE capital deployed in a single quarter, driven by large take-private activity in hard asset sectors, even as software posted an unexpectedly robust value share from several mega-deals announced before the SaaS valuation reset took hold.

(Past performance is no guarantee of future results.)

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…