- For Octus’ full analysis, please email directly.

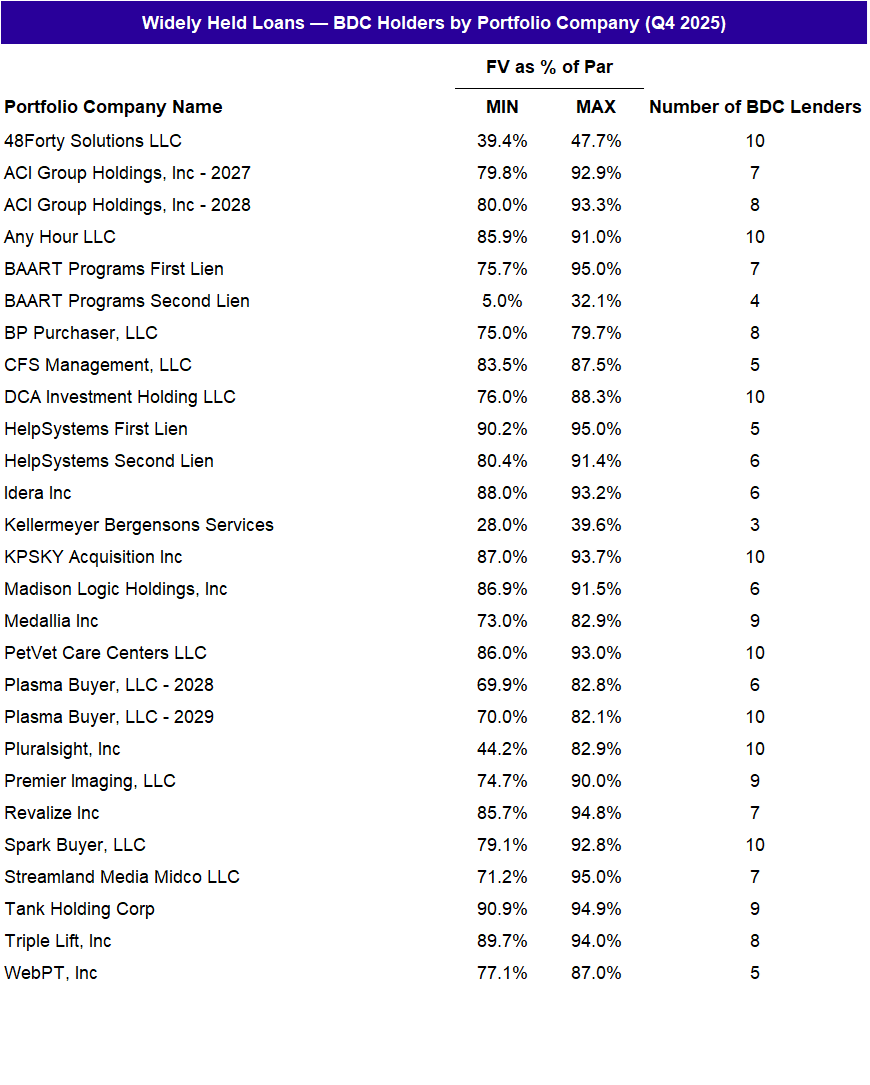

Octus analyzed 27 stressed securities across 23 borrowers and found that fair value pricing varied by as much as 40 points between the lowest and highest marks, with an average range of approximately 10 points as of December 31, 2025. BDCs managed by Blackstone and BlackRock tended to carry the lowest average prices in stressed club deals, while FS KKR exhibited the highest.

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…