")

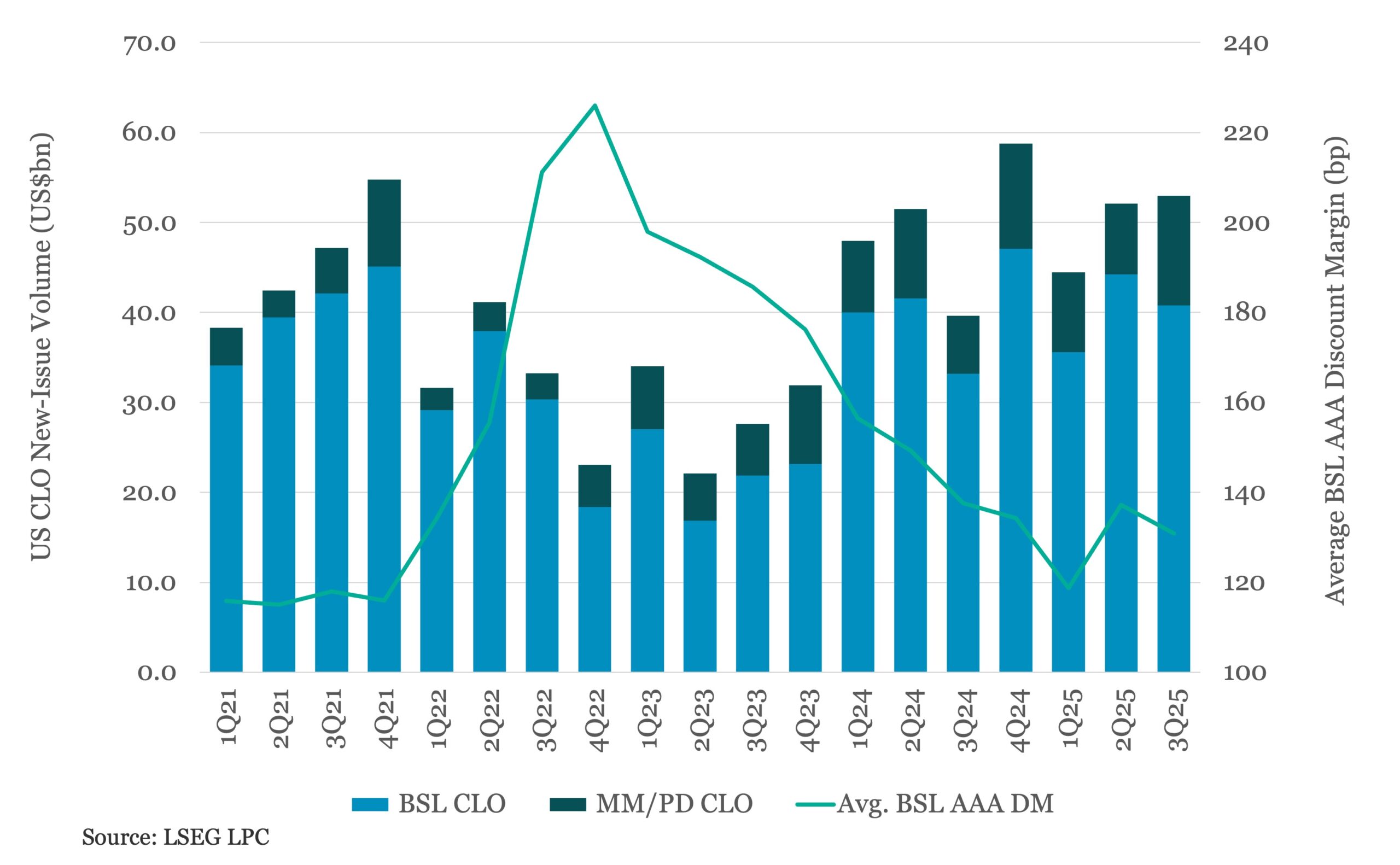

New-issue US CLO volume amounted to US$53bn in 3Q25 via 106 deals, up 2% from 2Q25’s US$52.1bn and 34% from 3Q24’s US$39.6bn, marking the highest quarter since 4Q24. Issuance was split between US$40.8bn of BSL CLOs and US$12.2bn of middle-market CLOs. This is the highest quarterly issuance for MM/PD since 2016. 1-3Q25 volume stands at US$149.6bn across 308 vehicles, 8% above the US$139.1bn raised from 295 deals during the same period last year. 3Q25 AAA discount margins tightened to 131bp from 137bp in 2Q. 3Q AAA discount margins are 7bp lower than levels seen a year ago.

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…