")

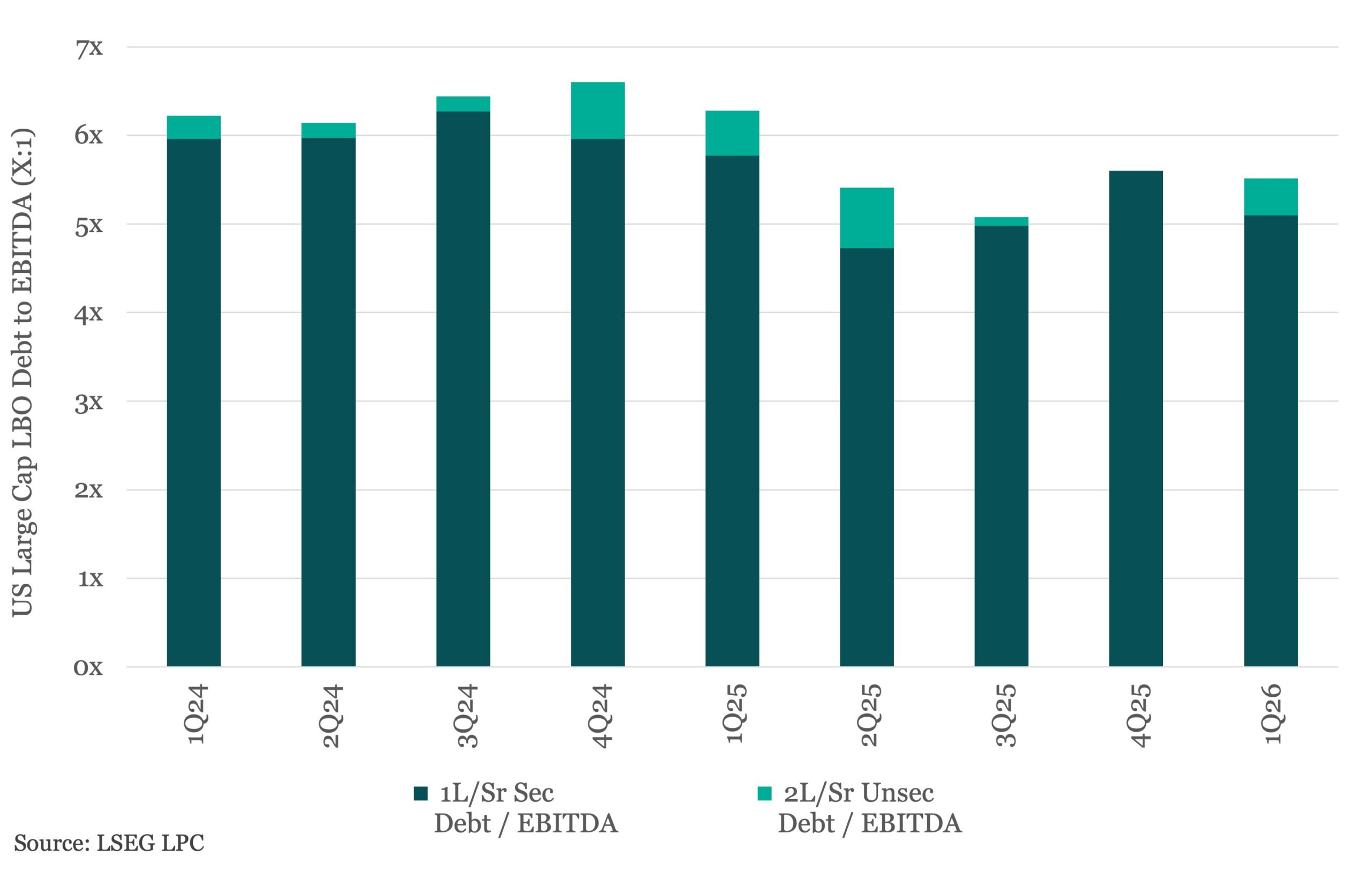

Although leverage multiples on recent large cap LBOs have eased marginally, averaging 5.5x in 1Q26 versus 5.6x in 4Q25, debt composition has shown signs of normalization. Junior-lien and/or unsecured debt accounted for nearly a half turn of leverage in the latest quarter, the largest contribution we’ve seen since 2Q25 and a shift from nonexistence throughout the back half of last year. The majority of buyout financings are still being structured with 100% senior secured first-lien debt supported with substantial equity cushion, although you’re starting to see some privately placed second-lien term loans and unsecured bonds in situations where such paper and economics make sense. That sometimes means rolling existing debt into the new capital structure, as was the case with Select Medical and to a much lesser extent Sealed Air. Electronic Arts was certainly the most notable new raise given its capacity-testing size and cross-border execution ($18bn total funded quantum with 80/20 split between dollars and euros), and provides a great reference point in showcasing relative value across the debt capital structure. The US$6.125bn dollar term loan B (7Y / S+350 / 98.5) printed with a 7.7% yield, or 43bp outside the US$2.875bn senior secured dollar notes (7Y / NC3 / 7.25%), while the US$2.5bn senior unsecured dollar notes (8Y / NC3 / 8.75%) printed 150bp behind the adjoining secured notes.

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…