Middle Market Deal Terms at a Glance – January 2025

Source: SPP Capital Partners Contact: Stefan Shaffersshaffer@sppcapital.com

Source: SPP Capital Partners Contact: Stefan Shaffersshaffer@sppcapital.com

Launched Volume Source: LevFin Insights New-issue Yields Source: LevFin Insights Weekly Fund Flows Source: Lipper (Past performance is no guarantee of future results.) Contact: Robert Polenbergrobert.polenberg@levfininsights.com

Average Free-and-Clear as a Multiple of Pro Forma Adjusted EBITDA (M&A-Related vs. All Deals) (Past performance is no guarantee of future results.) Contact: Steven Miller smiller@covenantreview.com

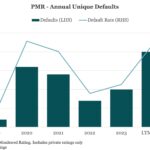

North America Private Credit Default Rates to Stabilize in 2025 Click here to learn more. Join Fitch for the upcoming Outlook panel: Credit Outlook 2025 Private Credit Rating downgrades and default rates for Fitch’s North America Privately Monitored Ratings (PMR) portfolio could stabilize in 2025…. Subscribe to Read MoreAlready a member? Log in here...

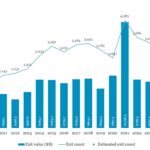

Global PE exit activity Download PitchBook’s Report here. 2024 recorded just under 3,800 completed PE exits, for an aggregate of over $900 billion (including estimations)…. Subscribe to Read MoreAlready a member? Log in here...

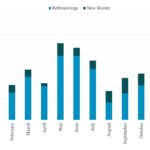

Nearly 83% of total 2024 US institutional loan volume represented refinanced credits Arrangers of leveraged loan debt kept busy in 2024, raising nearly US$1.7trn of issuance during the year…. Subscribe to Read MoreAlready a member? Log in here...

What we learned about 2024 is that many worries identified by analysts and market observers came to naught. Rates, economic growth, and inflation – all areas of concern last January – are in good shape as 2025 rolls out. More robust job growth than expected (see our Chart of the Week) is just one example….

December’s job adds topped expectations, suggesting slower Fed rate cuts. Source: WSJ, The Daily Shot

We resume our discussion of the private equity liquidity crunch and its impact on fundraising, this time from the LP’s perspective. The supply/demand imbalance in the fundraising environment has shifted to favor LPs. This gives them greater GP access, longer diligence windows, and more negotiating power with LPA terms. But many LPs, their investment programs […]

Direct lending the driver of private debt growth in Europe Read more in Preqin’s ‘2025 Global Report: Private Debt’. Since the Global Financial Crisis, direct lending AUM has grown at a faster rate than other private debt strategies in Europe, such that it now comprises more than two-thirds of private debt AUM (67.3%)…. Subscribe to