Investors are challenged today with so much data and distraction coming at them from every angle. This makes it tough to see the big picture, which looks pretty good.

After a dramatic 50 bp chop to the Fed funds rate barely two weeks ago, the mood has swung around once again. Now it’s more like,“What’s the rush?” Indeed, several panelists at the Greenwich Economic Forum last week suggested rates were at a good level, keeping inflation at bay and allowing the economy’s momentum to continue.

Our experience has been that most predictions of risks have the timing exactly wrong: buy when you should be selling, sell when you should be buying. Those who say credit is risky, for example, because interest rates are high, will miss the best of both worlds. Debt costs will improve for borrowers, but all-in yields for investors will remain well above historic levels.

There’s also the problem of perspective. Headwinds for some are tailwinds for others. This is most obviously true of how rates impact investors and issuers; low rates not great for the former, helpful for the latter. And headwinds today, whether rates or the economy, can be tailwinds tomorrow, next week or next year. Finally, headwinds for one asset class – say, bonds in a rising rate cycle – can be tailwinds for loans.

Understanding the interplay of these dynamics is instrumental to the popularity of private credit. The uninterrupted growth of the asset class over almost three decades of multiple business and rate cycles and pandemics is a testament to its resilience for investors and issuers.

What are the biggest surprises for investors this year? Our informal polling among top credit managers produced five answers. First, muted M&A activity, despite improved conditions for financing. Second, is the strength of the economy. Though rates have been high compared the zero-gravity era that ended in 2022, consumers keep spending and companies keep hiring.

Then there’s the resilience of credit portfolios. Rating agencies and investment banks forecast scary default numbers this year for private credit, higher than bank loans or junk bonds. Those never materialized. Also, market volatility related to the US election (“Is this it?”) has yet to emerge, though there will be plenty of time for post-election blues.

Who back in the depths of Covid would have foretold the strength of the S&P Index? From a relative low of 2500 in March, 2020, to 5800 today, a 132% rise. Including over 20% last year and year-to-date. Throw in credit spreads at tights and you have a remarkably bullish picture. Proof once again that markets happen when you’re making other plans.

As a new rate cycle triggers a reassessment of which strategies deserve allocations, managers and investors struggle to identify winner and losers. How does the “everything happens so much” environment complicate these decisions?

Latest news

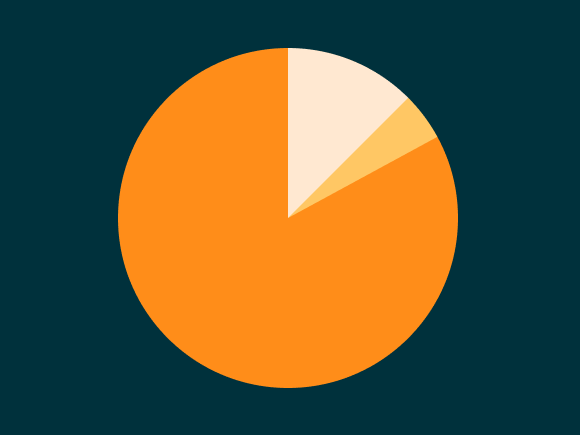

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…