Back to School

Our fondness for inflection points suggests there are many to consider. First, the economy. Despite many misgivings over the past eight months, US GDP growth has been remarkably solid. Second quarter numbers were revised upward from 2.8% to 3% in large part due to strong consumer spending. The third quarter is still hanging tough with estimates around 2%.

Yes, slowdown worries never seem far away. While a full-blown recession still appears unlikely, investors are anxious about any signs of softness. Weaker factory orders and a lower purchasing managers index checked that box this week…

▶︎ Read Sept 3rd, 2024 Newsletter: here

Latest news

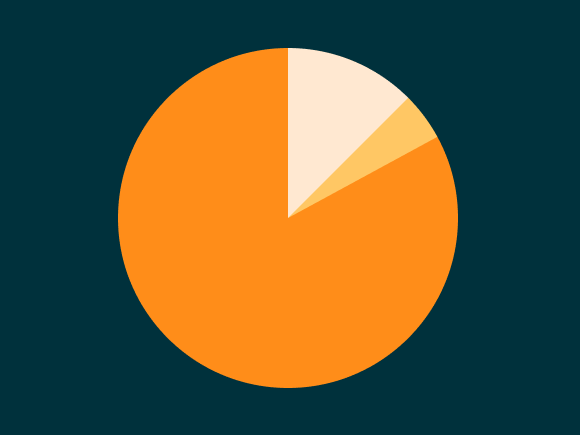

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…