CLO Awakening (Second of Two Parts)

From a risk perspective, CLO defaults are rare; no AAA tranche in either US or European CLOs has ever defaulted. The historical default rate for all CLO tranches is just 0.11%, and none occurred post-GFC until 2021. Then only after portfolios had been partially weakened from loan credit quality issues emerging during the Covid-19 pandemic.

In a similar vein, Barclays analysts reported that BSL CLO exposure to S&P-rated CCC assets dipped month-over-month. The median exposure fell to 6.2% in July from 6.5% in June. Only 27.1% of CLOs have in excess of 7.5% of CCC or below rated assets compared to 32.9% in June, according to Barclays.

▶︎ Read July 22nd 2024 Newsletter: here

Latest news

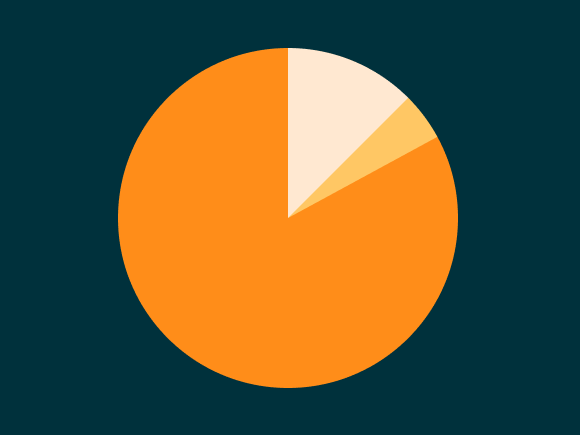

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…