Beyond structural pressures, liquidity mismatches, and conflation with large cap strategies, the most fundamental question for any credit investor: What is the actual risk of losing money?

Structural protections are built into core middle market (CMM) loans because they are illiquid and intended to be held to maturity. Unlike large cap cov-lite deals, CMM loans have financial covenants testing borrowers’ ongoing performance, meaning that lenders get early warning and intervention rights before the asset reaches the point of impairment.

Lower leverage is also a critical defense. When a borrower is capitalized with more equity and less debt, the distance between the enterprise value and the debt stack is larger. That equity cushion absorbs losses first. In a well-structured middle market deal, PE sponsors typically contribute 50 – 60% of the capital structure as equity. They are buying businesses where the valuation is supported by cash flow fundamentals, not multiple expansion or momentum.

Origination also matters as much as structure. Because CMM lending is relationship-driven – built on deep familiarity with sponsors, with industries, and with specific management teams across multiple transactions – lenders have informational advantages that are simply not available in a broadly syndicated or publicly traded context. They know their borrowers and understand the business model. When conditions deteriorate, those deep relationships make early detection and proactive management possible.

Broad diversification across service industry sub-sectors further reduces concentration risk. A CMM portfolio spanning business services, healthcare services, financial services, and technology-enabled businesses is not carrying the sector-specific risk that can accumulate in a large cap portfolio where the most competitive deals tend to cluster in exactly the industries everyone else is chasing.

None of this means CMM direct lending is not without default risk. Credit cycles are real, and no covenant or equity cushion makes a portfolio immune. But the default risk profile of a conservatively constructed, covenant-rich, lower-leverage middle market portfolio looks materially different from today’s headlines. Those headlines are shaped by large cap deal structures and retail-driven liquidity stress — not the CMM.

Institutional investors with long-term liabilities understood this from the onset. They matched the illiquid tenor of private credit with patient capital, held assets through cycles, and earned the yield premium that the illiquidity the asset class provides. The second golden age of private credit, if it comes, will belong to investors who approach the asset class with the same discipline — matching their time horizon to the asset, understanding the structural protections that make secured credit resilient, and resisting the temptation to conflate the OG of private credit with strategies that carry its name but not its principles.

Latest news

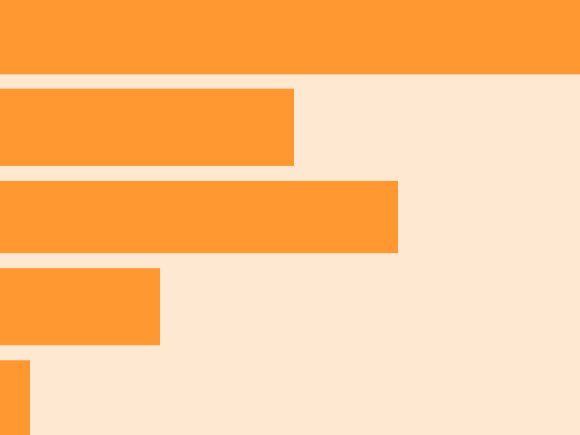

PE middle-market pooled IRR and TVPI by TEV size bucket

The lower end of the middle market has generated better returns on average and does not come with significantly more left-tail risk

Investors exit retail loan funds in July

Investors in leveraged loans have been pulling money from retail funds in recent weeks, with redemptions outpacing investments by $253.3b…