What’s so special about the middle market? In a world where every conversation seems to revolve around AI, mega-software M&A, and data center infrastructure, it is easy to overlook the arena that creates 30% of private sector employment and 33% of revenue growth. But as investors grapple with AI transition risks, elevated leverage, and weaker structures in large cap portfolios, the core middle market is getting second and third looks.

Pest control companies, veterinary clinics, and HVAC services aren’t featured on many prime-time business TV programs or conference agendas. But “old economy” sectors are commanding more attention from private equity buyers and their direct lending partners who specialize in core middle market companies. Purchase price multiples for these HALOs (heavy asset, low obsolescence) with cash flows in the $25 – 75 million range have risen to double-digit ebitda multiples, improving the cash equity share of buyouts and holding down leverage multiples.

Today’s industry composition of portfolios for the leading core MM direct lenders did not materialize over night. Those few private credit managers who lived successfully through the Great Recession learned some important lessons in those tough times. First, diversify. Keep watch on your outsized sector concentrations. No matter how much you may love dental practices, don’t build your entire portfolio with them.

Diversify by commitment size, particularly in the early stages of building a fund or portfolio. Nothing should be over 2% of the total AUM. That way an unexpected problem with a large exposure doesn’t kill your returns. Remember, credit investment success means getting your interest and principal back. Don’t reach for the moon when all you have is a stepladder.

Second, cyclical companies are what they say they are; in a recession, these businesses will be the first to feel the pain and sometimes the last to recover. In other words, if you plant nothing but crocuses in your garden, your landscaping will be pretty bare most of the growing season.

Emphasize commercial over consumer. Demand trends for the former are easier to predict than for the latter. We thought consumer brand names would carry the day during the GFC, as they did in prior turndowns, but it turned out value brands won out. With so many buying options available, the velocity of changing consumer tastes has never been more challenging to predict.

Finally, services over manufacturing. Specialized manufacturers can be excellent middle market businesses, but rising labor expenses and tariffs have made the input cost story more challenging. Not to say service companies don’t employ human capital. But the best of them have higher free cash flow margins that allow for more leverage and investment growth.

Private credit investors may see what’s in manager portfolios, but not always the history and knowledge behind the scenes. In this special series, we look at the history of business selection in the middle market. How the macro shapes sector allocation, how private equity expertise influences those decisions, and how top managers build all-weather portfolios designed to diversify and protect their investors.

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

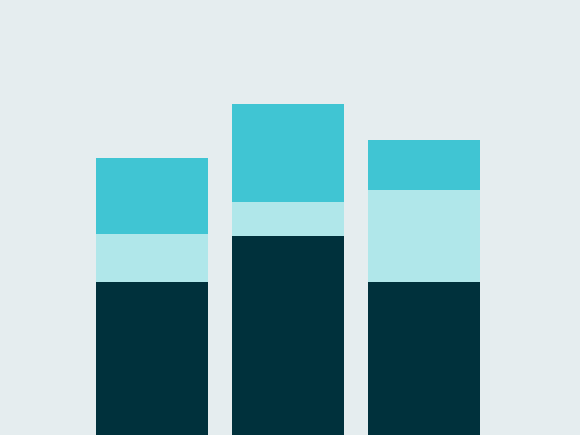

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…