The surprise of 2025’s post-Liberation Day risk-on dynamic across markets has established a pattern we expect to continue well into next year. As we discussed last week, the implementation of rate cuts, the slowing of inflation and the persistence of economic growth has supported dealmakers and their financing partners.

Nevertheless, attention is focused on transactions closed during the highest rate period from 2022 – 2024. It had been forewarned that defaults should be expected emerging from that time. And so now every story of a troubled deal triggers warnings of a coming credit crisis.

At a well-attended Investment & Pensions Europe webinar we were asked whether these failures are indicative of private credit deterioration. Are they changing how we evaluate companies? Bank-led deals and private deals in challenging sectors or with higher leverage are among those showing signs of stress. Direct lenders in the middle market are mostly dealing with “idiosyncratic” situations, with little evidence of portfolio-wide problems.

Key to sound portfolio construction is sourcing. The only way a bad deal gets into your portfolio is if you put it there. If deal flow comes from a basket of miscellaneous stuff with a wide range of risk outcomes, your selectivity needs to be perfect. If you instead start with a pre-screened list from top private equity firms, that’s a good start. If you are also an investor with those sponsors across hundreds of funds, the pool quality becomes even better.

Next, experienced managers filter the opportunity by industry. Easier said than done. Smaller company operating performance is tricky to predict and derailed by a host of circumstances. Leaders in niche sectors have built moats and fortresses around their businesses. The lender’s job is to figure out what can dent those defenses. Decades of underwriting practice helps.

The best managers are rewarded not to invest with unpredictable outcomes. Besides defaults, a key concern related to private credit is too much money chasing too few deals. Unless you are extremely disciplined, the tyranny of having excess dry powder (i.e. unused cash raised from investors) will result in sub-optimal choices for the sake of putting client money to work.

This is really a question of differentiation. The US middle market is distinct from the large cap market because successful businesses inhabit smaller specialized sectors. These niche service industries have proven to be resilient over a range of business cycles. Examples include healthcare, software, logistics, technology, and business services such as accounting firms, commercial landscaping, HVAC, pest control, and fire suppression.

There are over 200,000 middle market companies, representing almost half of GDP and hiring. Only 5% are owned by private equity firms, leaving a wealth of growth prospects. Financings come from a small club of lending partners with little overlap. Being able to handpick the best opportunities means you can pass along the highest-quality pool to your investors.

Latest news

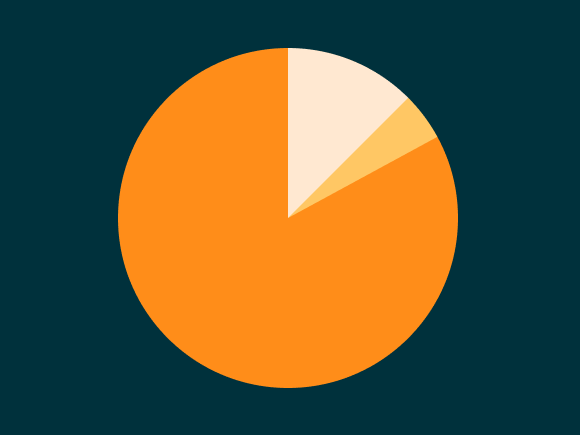

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…