Click here to download report.

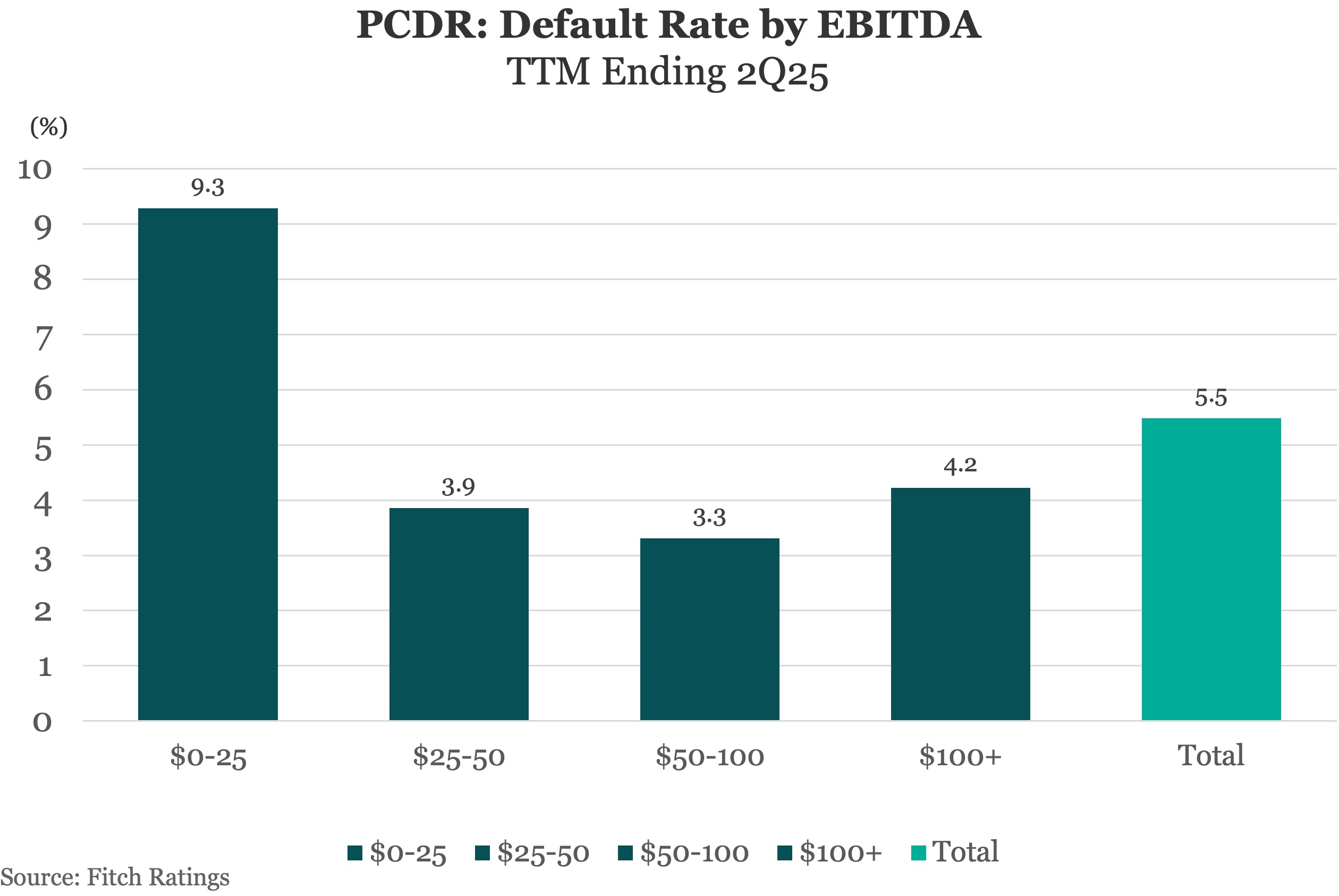

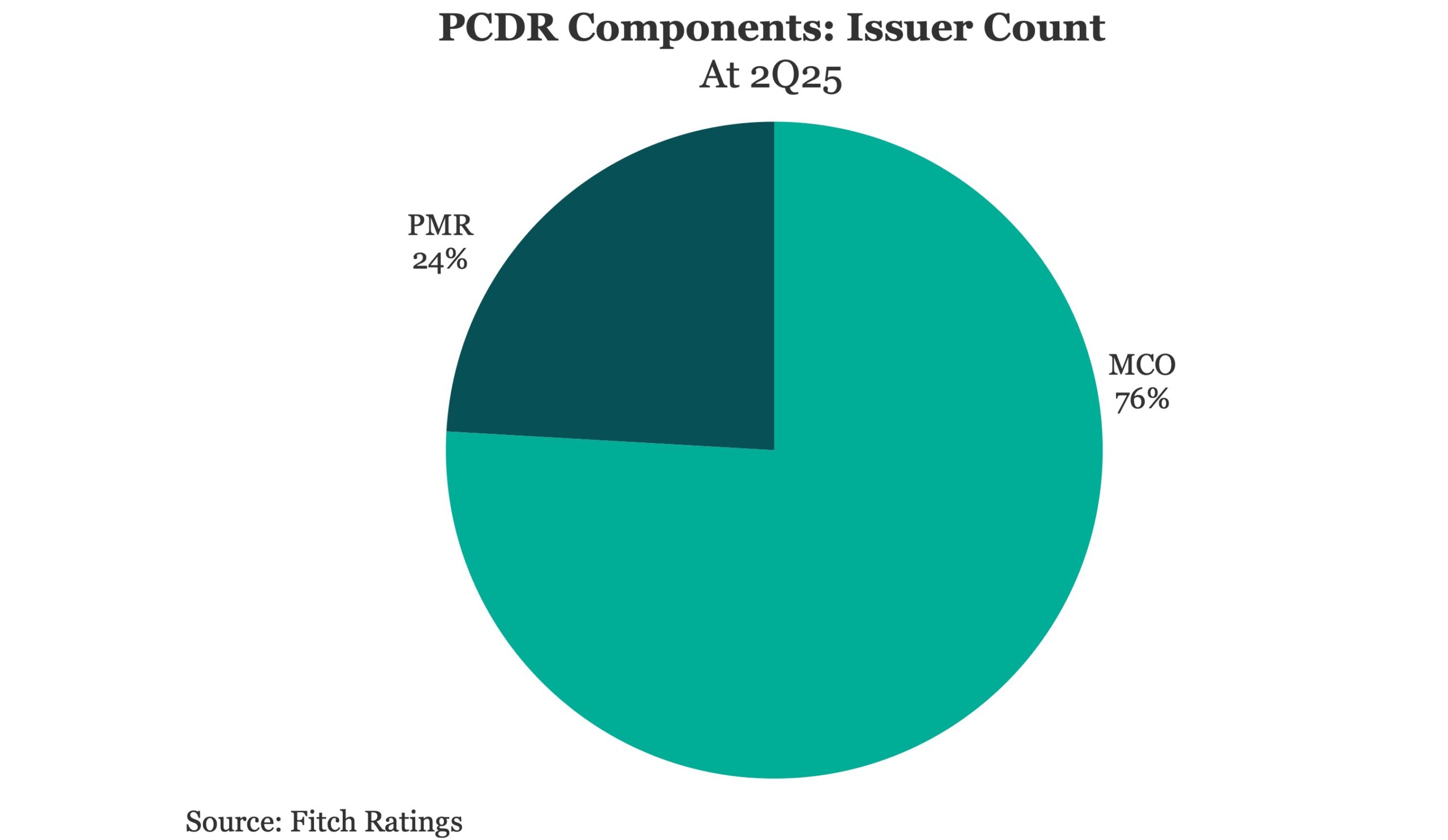

Small issuers generating less than $25 million EBITDA defaulted at more than double the rate of larger issuers in Fitch Ratings’ Private Credit Default Rate (PCDR) universe during the trailing twelve months (TTM) to 2Q25. This report examines private credit defaulters by EBITDA size, compares default rates across the two component Model-based Credit Opinion (MCO) and Privately Monitored Ratings (PMR) portfolios, and details default reasons.

Latest news

Q2 European direct lending activity up 9%

Despite the geopolitical and macroeconomic events of the first half of the year creating a volatile environment, the European private credit market continues to demonstrate robust resilience.

Share of PE middle-market fund count by size bucket

Sector composition tilted hard toward B2B in Q1. B2B accounted for 52.9% of middle-market exit value, up from 38.2% in full-year 2025…

US Leveraged Loans return 1.88% to investors YTD

The Bloomberg US Leveraged Loan Index (Ticker: LOAN) has returned 0.57% to investors this month through July 15, bringing the…