Chart of the Week: Security Issues

The prospect of lower interest rates has boosted new CLO issuance at a record pace. Source: CreditFlux(Past performance is no guarantee of future results.)

The prospect of lower interest rates has boosted new CLO issuance at a record pace. Source: CreditFlux(Past performance is no guarantee of future results.)

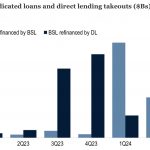

Refinancings by direct lenders returned last quarter to outweigh BSL takeouts. Source: PitchBook LCD, data through June 30, 2024(Past performance is no guarantee of future results.)

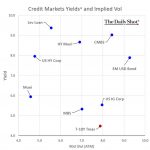

Among a basket of traded credit strategies, leveraged loans are showing well. Source: The Daily Shot(Past performance is no guarantee of future results.)

Consumers gloomy, but keep pushing stock prices higher. Source: Bloomberg, The Conference Board(Past performance is no guarantee of future results.)

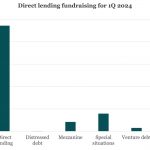

Private capital fundraising for the first quarter was predominantly for direct lending. Source: Preqin Pro(Past performance is no guarantee of future results.)

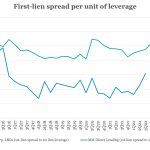

Middle market direct lending spreads per unit of leverage consistently higher than large caps. Source: LSEG LPC(Past performance is no guarantee of future results.)

Distributions to LPs are severely hampered by slower M&A activity since Covid. Source: Ares Management, Goldman Sachs(Past performance is no guarantee of future results.)

Lower earnings activity is not always synchronized with worse economic performance. Source: Nuveen Multi-Asset, Bloomberg monthly S&P trailing 12 month EPS YoY; National Bureau of Economic Research Economic Recession Indicator from Jan ’54 Mar ‘24(Past performance is no guarantee of future results.)

Repricings, refinancings, and extensions hit record volume in the BSL market. Source: PitchBook LCD(Past performance is no guarantee of future results.)

Since the Fed’s rate hike regime began, more bankruptcies are reorganizations. Source: Torsten Slok – Apollo, The Daily Shot(Past performance is no guarantee of future results.)