Chart of the Week: On A Roll

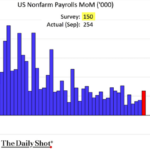

September’s surprisingly strong jobs report further signals a soft landing. Source: The Daily Shot(Past performance is no guarantee of future results.)

September’s surprisingly strong jobs report further signals a soft landing. Source: The Daily Shot(Past performance is no guarantee of future results.)

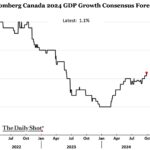

Canadian GDP forecasts have been increasingly bullish since January. Source: The Daily Shot, Bloomberg(Past performance is no guarantee of future results.)

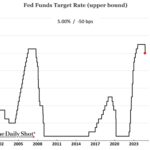

The size of the Fed’s first rate cut in over four years – 50 bps – surprised analysts. Source: The Daily Shot(Past performance is no guarantee of future results.)

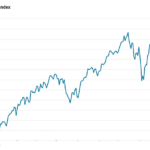

Since early July public equities have seesawed between recession worries and confidence. Source: FactSet(Past performance is no guarantee of future results.)

Consumers in Italy reported a drop in confidence last month. Source: The Daily Shot(Past performance is no guarantee of future results.)

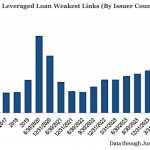

The number of negative watch or warning leveraged loan borrowers is declining. Source: PitchBook | LCD; Morningstar LSTA US Leveraged Loan Index (Past performance is no guarantee of future results.)

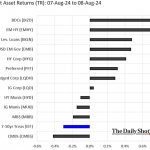

Amid last week’s turmoil in public equities, loan and bond returns thrived. Source: The Daily Shot(Past performance is no guarantee of future results.)

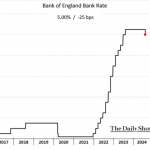

The Bank of England lowered its benchmark rate for the first time since Covid. Source: The Daily Shot(Past performance is no guarantee of future results.)

The UK has been the main source of European private debt deal volume. Source: Deloitte Private Debt Deal Tracker, Spring 2024(Past performance is no guarantee of future results.)

New CLO issuance in Europe this year is outpacing 2023 by a wide margin. Source: Pitchbook | LCD(Past performance is no guarantee of future results.)