Chart of the Week: Inventory Check

Private equity remains an attractive option for investors through cycles. Source: Pitchbook

Private equity remains an attractive option for investors through cycles. Source: Pitchbook

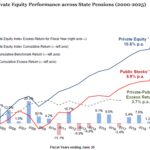

For over two decades private equity has outperformed public stocks in state pension plans. Source: Cliffwater

While PE deals transacted shrunk since 2021, deal values rose over past three years. Source: PitchBook

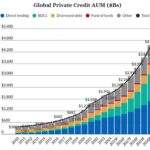

Direct lending and BDCs expected to lead the growth of private credit. Source: Fitch Ratings

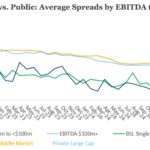

The private credit yield advantage over BSL widens as single-B spreads shrink. Source: KBRA DLD Research, PitchBook LCD

Defaults for the overall leveraged loan market are at lowest point since 2023. Source: The Daily Shot, PitchBook/LCD, Morningstar LSTA US Leveraged Loan Index

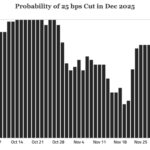

A low probability just weeks ago, chances for a 25 bp cut now seem likely. Source: The Daily Shot

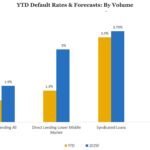

Direct lending defaults lead credit categories in low defaults, though headed higher. Source: KBRA DLD Default Research

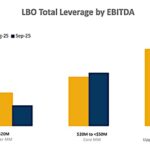

Larger LBO financings in direct lending are sporting increasingly higher leverage. Source: KBRA DLD Research, 3-month rolling averages

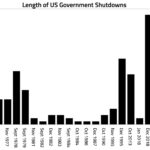

On November 5th, the 2025 government shutdown became the longest in US history. Source: The Daily Shot