A year ago we identified four issues for 2024 that would lay the foundations for a Goldilocks era in private debt and private equity:

- How a recalibrating market will accommodate the new higher normal for interest rates.

- Why dispersion between winners and losers looks set to increase.

- Why portfolio performance will rely on diversification across high quality issuers, industries, and asset classes, combined with alignment with top private equity owners.

- How private capital providers’ increasingly sophisticated financing tools will meet the market’s complex needs and generate strong risk-adjusted returns for investors.

It turns out all these factors did contribute to a stellar year for top private capital managers and investors. As we look back at the market’s progress, it’s now evident the macro concerns we had going into 2024 were mostly resolved by year’s end. Rates? Coming down, but not in any rushed fashion. The economy? No recession here (goodbye, inverted yield curve), solid growth, not too hot. Inflation? Pretty tame. Unemployment? Still near multi-year lows.

We also have hopeful answers to last year’s market worries. Would M&A flow pick up with the prospect of lower interest rates? Yes, 3Q was the turning point, and BofA predicts 23% more “event-driven” activity for 2025. Heightened private credit risk? Didn’t happen; in fact, direct lending defaults were 1.5%, according to KBRA, about half of what they projected.

Increased competition between banks and private credit leading to weaker terms? Not in the middle market, where terms remained investor-friendly. Yes, all-in spreads contracted, but more pronounced at the upper end of the market and for large cap financings. And despite warnings that banks would erode private credit market share, leading direct lenders reported anywhere from 20-30% better volume last year than in 2023. And some had record volume, even compared to 2021. All while the leveraged loan market hit a record $1.5 trillion.

It’s clear both public and private credit markets can co-exist without damaging each other or their investors. In their 2025 outlook piece, S&P called this “The Great Convergence.” This effect was more evident with issuers greater than $100 million Ebitda. And the ability of banks to mimic hold capabilities of leading direct lenders is limited. Nevertheless, both banks and non-banks are now freely transacting across a variety of deals.

Next week we begin a new series examining five themes characterizing our outlook for 2025:

- Still higher for longer: What slower rate cuts mean for private capital investors.

- Busier markets: How to source and secure high-quality opportunities as activity grows.

- Default positions: Can discipline and careful portfolio construction keep portfolios clean.

- Platform excellence: What today’s highly selective LPs look for in a manager.

- Fresh air: How exits, fundraising and new deals will develop through 2025.

Latest news

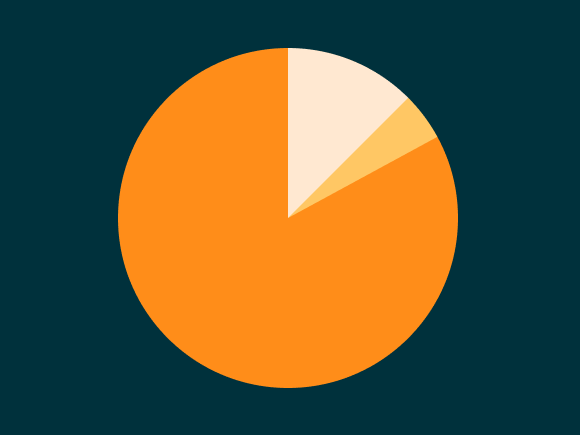

Multiples on PE buyouts

This quarter marks our integration of SPI by StepStone as the primary source for US buyout valuation metrics for the PE Breakdown.

US Leveraged Loan Issuance Slows to $76.5b in July

The US leveraged loan market has continued to slow from the May level of $104.7b, with approximately $76.5b priced in…